Online and onward!

E-commerce

The forty year history of e-commerce has been a story of impressive growth – and this trend is more than likely to continue. In 2016 e-commerce in Europe is expected to generate app. EUR 509.9 bln of online sales of goods and services. According to the European B2C E-commerce report by Ecommerce in Europe, this figure will signify growth of 12 pct y-o-y, slightly less than the 13.3 pct growth of 2015. This surge in online sales is way above the growth of general retail in Europe, which in 2015 came to just 1 pct. “According to the various reports that have been published, the e-commerce segment is growing at a rate of 12 pct to 15 pct per year. This very positive trend should continue for at least a couple of years,” says Robert Pawłowski, a senior industrial and logistics negotiator at CBRE.

Direct leases the majority

How is this exponential growth affecting the industrial property market? Prologis’ research includes a detailed lease-by-lease review to quantify this growth. The authors of the report, entitled European E-commerce, E-fulfilment and Job Creation, analysed all the new leases across ten European countries over three years (2012–2014). These included the UK, Germany, France, the Netherlands, Spain, Italy, Sweden, Poland, the Czech Republic and Hungary. According to the research, 5 mln sqm of new e-fulfilment leases occurred at that time. Out of this, 3.4 mln sqm were direct new leases – a category fairly straightforward to track. “For 3PL leases, we conducted a ‘deep dive’ of our own portfolio to understand the e-commerce demand that could surface in this category. Our data suggest it equates to app. 50 pct of direct leases. Therefore, we estimate that 3PLs account for 1–2 mln sqm of additional e-commerce demand. For omnichannel leases, e-commerce related demand is not quantifiable and as such represents an incremental upside to our demand estimates,” explain Prologis’ researchers in the report.

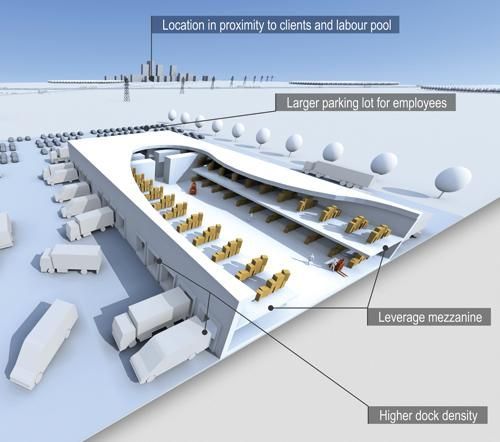

Proximity to people counts most

The top three countries for direct lease e-fulfilment are the main consumption markets, with 28 pct of direct leasing occurring in Germany, 22 pct in the UK and 16 pct in France. Cost-efficient fulfilment markets round off the top five markets, including Poland (13 pct of direct leases) and the Czech Republic (9 pct). Leasing in these countries reflects the opportunity for more cost-efficient labour as well as important new growth markets for the e-commerce sector. “Finding qualified employees is and will remain one of the key location criteria for online retailers. Being located close to metropolitan areas offers the best opportunities for finding new employees with a range of qualifications and affiliated services,” states the report.

Around 75 pct of direct leases were in metropolitan areas with populations above 1 mln, so the proximity to people – either consumers or the labour supply – are a key location consideration for e-fulfilment operations. Transportation costs are critical for location strategies within markets. Site selection comes down to evaluating the proximity to customers, the availability of labour and the proximity to the distribution networks of parcel and express carriers. The best sites offer a balance of these requirements, allowing e-fulfilment operations to staff their operations, to enjoy rapid deployment of deliveries and to manage transportation costs. Locations close to urban areas are well-positioned for the e-commerce sector.

“The ability to lower transportation costs and improve customer service, via proximity to the end consumer, has and will continue to be a key factor for e-commerce requirements,” predict Prologis’ experts. Locations within or near metropolitan areas are likely to benefit the most. Modern logistics hotspots are expected to attract the most demand from medium and large-sized retailers, while first-generation business parks are expected to bring in smaller retailers.

One size doesn’t fit all

There is the perception that e-commerce only requires new and large facilities, but the data tell a different story. Almost 60 pct of new direct leases were in units below 40,000 sqm in the past three years. In contrast, just 25 pct was signed for large-scale units above 75,000 sqm. This distribution follows naturally from the diverse nature of the online retail industry, which comprises a wide range of large and small retail concepts. Out of this diversified demand, half were new facilities and half were satisfied by existing assets. However, there is a substantial difference in terms of size; smaller leases tend to be in existing assets, whereas large leases are often in newer assets. These relatively high ratios of leases in the existing stock show that e-commerce requires a specific set of requirements, but these can mostly be addressed by generic logistics real estate.

In practice, the demand can be segmented into two types of requirements, which include infill facilities for last-mile delivery and larger requirements for regional e-fulfilment. For infill requirements, last-mile delivery focuses on locations and business parks close to city centres. These requirements tend to be smaller (less 10,000 sqm) and can be met with existing facilities. For regional e-fulfilment requirements, traditional locations for modern logistics facilities generate the most demand. These locations offer a variety of unit sizes and features (e.g. coverage ratios and ceiling heights), proximity to key infrastructure nodes, and locations that balance their transportation, labour and real estate cost structure. Traditional e-commerce demand has generally been concentrated in the regional e-fulfilment category; however, the growth has recently become more pronounced for infill last-mile facilities.

Return processing centres most needed

According to different research by Prologis, prepared in partnership with JLL, new e-commerce driven take-up in Poland is likely to amount to up to 700,000 sqm over the next five years. This would also make it one of the key drivers of the industrial and logistics market across the country. According to PMR, between 2012 and 2014 Poland’s e-commerce sales were increasing on average by PLN 3 bln per year. The research reveals that each additional billion złoty spent online generated warehouse demand of app. 18,500 sqm.

The authors of the report also asked 3PLs and retailers what kind of e-commerce related warehouse functions they will require over the next five years. Returns processing centres were the choice of 71 pct of 3PLs and 36 pct of retailers as the number one type of function they will require. The second most popular were e-fulfilment centres (3PLs – 71 pct, retailers – 18 pct) and the third most popular option were parcel delivery centres and urban logistics depots (3PLs – 41 pct, retailers – 18 pct). “Traditional retailers who engage in omni-channel sales are facing decisions such as whether to fulfil online orders from central hubs, from separate facilities, from stores, or through a hybrid solution. This largely depends on the volume of online sales and whether it is large enough to warrant a separate facility. Larger retailers who already operate in-house logistics and run their own distribution centres could consider handling both individual and store orders in the same facility,” states the report.